Achieve Life Sciences: Nicotine Cessation Drug with Short-Term Multi-Bagger Potential

Rogue Funds is officially trying to catch both sides of the nicotine addiction cycle for its investors. As always, ensure you read the disclaimer at the bottom of the post. Achieve Life Sciences ($ACHV) is a biotech company with two phase 3 trials under its belt and a best in class smoking cessation drug that in our view has the potential for billions in revenue (and IP protection through 2040). They are currently undergoing a long-term 52 week safety trial that will lead to a New Drug Application around the 1st half of 2025. This is a short post but it’s fairly straight forward and there’s nothing complicated about this. If you get a chance I highly suggest you check out Dalrymple Finance who have created a more in depth and more bullish report than I have!

The Drug

Achieves prized possession and its only product is Cytisinicline, a drug that has been approved and used for smoking cessation in Eastern Europe. Achieve has created a deal with the manufacturer to commercialize the product in the US and it has IP protection out to ~2040. It will hopefully replace the prior leading smoking cessation drug, Chantix.

How effective is it?

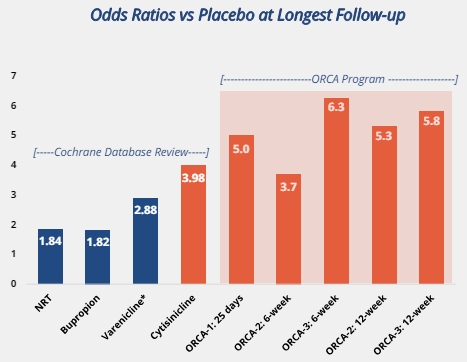

For a little background on smoking cessation: over 70% of smokers want to quit, 55% attempt to quit each year, and exactly 7% successfully quit each year. The current leading drug for smoking cessation (and the only drug approved since 2006 for smoking cessation) was Chantix (Varenicline) which was distributed by Pfizer. The odds ratio (or the multiple of success vs placebo) for Chantix was 2.88 for a 12 week trial (meaning you had a 2.88 times better chance of abstinence vs placebo).

For comparison, Cytisinicline has an odds ratio of 3.7 for its 6 week trial and odds ratios of 5.0-6.3 for its 12 week trials. See below for a visual comparison:

I won’t go into the breakdown of each of the ORCA trials but you can view them on the website where the go into a bit more detail but the important parts are the 6 week vs the 12 week results in ORCA-2 and ORCA-3. All studies had roughly the same smokers who roughly followed the below profile:

These are smokers who have tried and failed to quit numerous times and have been smoking for 5+ decades on average and the drug is having tremendous effects.

It is extremely obvious that Cytisnicline blows Chantix out of the water when it comes to efficacy and they are obviously the best in class. The next question is if they are actually safe?

How safe is Cytisnicline?

To be completely blunt, it is the safest drug and causes the least side effects of any smoking cessation drug on the market. First let’s compare it to placebo:

In comparison to placebo the real big knock is insomnia and abnormal dreams, which although that is a downside, it is not much above placebo and it performs great for the most “invasive” side effect that cause a user to stop using (nausea). I’ll explain this further when we compare to Chantix:

As you can see the adverse events vs Chantix are better in every single category and are very statistically significantly improved in nausea which was the number one event that caused Chantix users to quit their usage early. So although we have a drug that causes slightly more side effects than placebo it is drastically better than Chantix in nausea and better in every other adverse event category. The reason why the side effect profile vs Chantix is so important is because it is estimated in studies of real world use that only 20%-40% of users actually completed their whole Chantix regimen and 20%+ of users quit specifically because of side effects. A more effective and less intrusive drug could lead to much higher success rates for users (and possible expansion of the applicable population). We won’t take expansion of TAM into account though because every analyst in biotech thinks TAM will expand.

So to summarize we have a drug that works much better (even in a shorter duration) and is much safer than the leading drug in the category. Chantix generated over $850m in revenue in the US in 2019 alone and current generic version makes $430m a year.

Valuation

Roughly 14m people a year try to quit smoking and of those roughly 1.4m take a prescribed medication. The current generic drug course runs about $475 and Cytisinicline could probably push a much higher price probably close to $700-$800 based on how Pfizer was able to sell Chantix. If we assume a 30% market share (which isn’t as high as I think it will go) which would be about $300m in revenue per year and this implies a valuation of ~$1B (just over 3x sales). With a 60% market share this would imply $600m in revenue and a 1.8B valuation at 3x sales.

Currently the company sits at 55m shares diluted ($286m market cap adjusted for diluted shares outstanding and $5.15 share price as of this writing) with $64m in cash currently and another possible $60m+ from warrants. They now have more than enough cash to get them through this final NDA trial (they can apply for the NDA after 6 months of this trial which begins this quarter). This leaves the company with a very conservative valuation of ~3x-6x their current valuation ($15/s-$30/s). This is, again, a very conservative valuation as Chantix was able to produce $1B in revenue at its peak 5 years ago. It’s also cheap when considering IP lasts until 2040 and it’s been the only smoking cessation drug in nearly 20 years.

Dilutionary Woes and Poor Management led to Opportunity

Due to various funding disasters and poor management the company has taken a beating in the past which allowed them to become very cheap. First was the Silicon Valley Bank disaster which led to dilution and then a huge surprise from the FDA where they hit the company with a surprise long term study (you can view this request here). The FDA probably took this action due to the warning label they had to apply to Chantix after approval and did not want to repeat that debacle. The surprise study led to another surprise dilution event as the company had to fund this new trial from February of this year. The company is now fully funded into 2H 2025 with an expected NDA filing in 1H 2025.

Buyout is Probable

The main goal of the company is going to be a buyout. They have no salesforce or manufacturing and I highly doubt shareholders want to go through the dilution needed to achieve this. Based on the new investment banker board members and the CEO’s comments on calls talking about looking for a “global partner” it seems fairly obvious this will be a buyout. I recently met the CEO at a conference and a question was asked if this was expected to be a buyout and the CEO did not say it outright but it felt like he considered it a likely course of action due to this being a “one product company”.

Conclusion

With the above assumptions, I believe the company will most likely get bought out. With the last trial beginning, the NDA nearing, and JAMA posting about their successful Vaping Cessation trials, it feels like the price will begin to climb in the near future. I find the upside to be immense at this point and I believe the current long term study will at most cause another warning label and most likely won’t lead to a lack of NDA (FDA is mainly looking at the risk on prolonged users who relapse and take the drug again, not barring the drug completely). Unless some completely unknown extreme side effect occurs then I believe this company has a ton of upside with minimal dilution risk. Eventually a bidding war will begin to take place and there is a very strong chance the company is sold for $12/s - $25/s.

Disclaimer: The author of this idea and his Fund have a position in securities discussed at the time of posting and may trade in and out of this position without informing the reader.

Opinions expressed herein by the author are not an investment recommendation and are not meant to be relied upon in investment decisions. The author is not acting in an investment adviser capacity. This is not an investment research report. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is illustrative in nature, limited in scope, based on an incomplete set of information, and has limitations to its accuracy. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies' SEC and CSA filings, and consult a qualified investment adviser. The information upon which this material is based was obtained from sources believed to be reliable, but has not been independently verified. Therefore, the author cannot guarantee its accuracy. Any opinions or estimates constitute the author's best judgment as of the date of publication and are subject to change without notice. The author and funds the author advises may buy or sell shares without any further notice.

This article may contain certain opinions and “forward-looking statements,” which may be identified by the use of such words as “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential,” “outlook,” “forecast,” “plan” and other similar terms. All such opinions and forward-looking statements are conditional and are subject to various factors, including, without limitation, general and local economic conditions, changing levels of competition within certain industries and markets, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors, any or all of which could cause actual results to differ materially from projected results.